Card services

Apply for UOB Credit Cards to Enjoy Exclusive Rewards, Cashback Offers and Privileges.

Find out more

Our Investment Solutions

Our Unique Wealth Approach

Access the expertise of UOB Private Bank’s CIO in Singapore.

Invest in funds powered by Private Bank CIO– the United CIO Income Fund and United CIO Growth Fund.

Find out more

UOB TMRW

Meet UOB TMRW. The all-in-one banking app built around you and your needs. Bank. Invest. Reward. Make TMRW yours.

Find out more-

you are in Personal Banking

For Individuals

Wealth BankingPrivilege BankingFor Companies

Wholesale BankingFOREIGN DIRECT INVESTMENTAbout UOB

ABOUT USUOB GroupUOB NEWSCAREERSUSTAINABILITYUOB Subsidiaries

UOB Subsidiaries

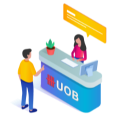

Product Highlights

Coverage for fire and additional perils

Includes fire, burst pipes, water leakage, and natural disasters such as earthquakes, floods, and windstorms

Flexible coverage plans

with 24/7 nationwide emergency assistance

Rental fee coverage for temporary accommodation*

*Subject to Coverage Section 1

Insured by

![]()

Table of Benefits

Insurance Details

Details

Insurance Coverage Period

- 1 Year 3 Year or 5 Years

Premium Payment Period

- 1 Year 3 Year or 5 Years (The policy is renewed according to the insured period.)

Premium Payment Mode

- Annually

Terms and Conditions

- If there are any materials misdescription of the Property hereby insured, or of any building or place in which such Property is contained, or of the use of such building or any misrepresentation as to any fact material to be known for estimating the risk, or for fixing the premium, or any omission to state such fact, this insurance contract shall be voidable and the Company have the right to cancel this Policy within the period as stipulated by law.

- The company reserves the right to decline the risk if the building construction is wood or timber.

- The Company reserves the right to revise the premium if the insured’s premises are located in a dangerous zone as announced by the Office of Insurance Commission (OIC).

Important Exclusions

- This coverage section does not cover the following properties: (unless otherwise expressly agreed and stated in the Policy.)

- Bullion or precious stones, jewelry or precious stones, or precious metals

- Any antique or work of art for an amount exceeding THB 10,000

- Manuscripts, plans, drawings, designs, patterns, models or moulds

- Securities, obligations, important documents of any kind, stamps, coins, paper money, cheques, or other business documents

- Explosives

- Electrical appliances and equipment, panels, electronic equipment, electric wires, or bulbs of which loss or damage is arising from or occasioned by over-running, excessive pressure, short circuiting, sparking, burning from electric wiring itself, leakage of electrical current including inherent vice or working

- Mobile phones, portable computers and/or electronic equipment, portable communication devices and/or cameras, video cameras and/or recording media of any kinds.

- All vehicles either on land, waterborne or airborne

- Trees, decoration of gardens and lawns

- Damage or any expenses incurred directly or indirectly whatsoever resulting and arising therefrom or any consequential loss directly or indirectly caused by or contributed to by or arising from war, invasion, baleful act of foreign enemy, or war-like operation whether war be declared or not, civil war amongst people in the same country, uprising, rebellion, revolution, coup d’etat, martial law, or any of the events or causes which determine the proclamation of maintaining martial law, political violence, act of terrorism, sabotage, strike or riot whether or not politically involved, any malicious act for the political, religious or ideological purposes.

- Acts of terrorism, which include acts or a series of acts to the use of force or violence or the threat thereof, of any person or group(s) of persons, whether acting alone or on behalf of or in connection with any organization(s) or government(s), committed:

- for political, religious, ideological or similar purposes, or

- to influence the government or put the public, or any section of the public, in fear

Additional Clarifications

Property Insured means

Building (excluding foundation) and/ or its contents including property contained within the insured premises as stipulated in the Policy Schedule.

Building (excluding foundation) means

Single house, townhouse, twin house, block-house for dwelling, parking lot and small outside buildings such as houses for servants, canteens and so on, walls, fences, gates including improvements excluding foundation. Room unit for dwelling within a condominium, flat or apartment excluding foundation.

Its Contents means Furniture, fixtures, fittings, tools, household utensils, electrical appliances and equipment, musical instruments, audio equipment, kitchenware, clothing and other property in the dwelling of the Insured or normal dependents (which are not specifically excluded in the Exclusions)

Warnings

All conditions, coverages, and exclusions are as specified in the insurance policy. The amounts of coverages and benefits depend on the insurance plan. Once you receive the insurance policy, please study the insurance terms and conditions in the policy.

Channel for Complaints by the Insured

The insured can file a complaint through the following channels:

- MSIG Insurance (Thailand) PCL. 1908 MSIG Building, New Petchburi Road, Bangkapi, Huaykwang, Bangkok 10310 Tel. 0 2825 8700

- United Overseas Bank (Thai) PCL, any UOB branch or UOB Contact Centre at Tel. 0 2285 1555 or www.uob.co.th

- Office of Insurance Commission (OIC), OIC Hotline 1186

- Bank of Thailand (BOT) Financial Consumer Protection Center, Call 1213 or Email: fcc@bot.or.th

United Overseas Bank (Thai) PCL is only a non-life insurance broker (Non-life insurance license number ว00020/2546). It serves to point out channels and manage people to enter non-life insurance contracts only. The insurance products are insured by MSIG Insurance (Thailand) PCL which is responsible for conditions, coverages and benefits according to the conditions specified in the insurance policy.

The applicant must study coverage details and conditions before applying for the insurance policy.

FAQ

Is the Insured permitted to determine the sum insured?

There are 2 types of basis of sum insured criteria:

- Replacement Cost Valuation

- Actual Cash Value

What does MSIG Baan Than Rak insurance cover?

A: Covers a total of 5 sections:

Section 1: Fire & Additional Perils

Section 2: Burglary, Theft, Robbery, Gang-Robbery (with forcible entry to or exit from insured building)

Section 3: Plate Glass

Section 4: Public Liability

Section 5: Personal Accident

Can tenants purchase MSIG Baan Than Rak insurance plan?

If the tenant has an interest in the insured property, such as furniture and other property for living, the tenant can take out insurance for this part. For buildings, the tenant can take out insurance by naming the lessor as the beneficiary of the building. Because generally, the house lease agreement will specify that the tenant is responsible for damages to the rented property.

Does MSIG Baan Than Rak cover wooden house?

The company reserves the right to decline if the building or structure is constructed entirely of wood.

Which documents are required for apply MSIG Baan Than Rak insurance?

The documents include an insurance application form and a copy of the insured's national ID card.

Connect with Us

UOB Contact Centre

Contact Us

Locate us

Drop your information for contact back.

Click!

We use cookies to improve and customise your browsing experience. You are deemed to have consented to our cookies policy if you continue browsing our site.