Card services

Apply for UOB Credit Cards to Enjoy Exclusive Rewards, Cashback Offers and Privileges.

Find out more

Our Investment Solutions

Our Unique Wealth Approach

Access the expertise of UOB Private Bank’s CIO in Singapore.

Invest in funds powered by Private Bank CIO– the United CIO Income Fund and United CIO Growth Fund.

Find out more

UOB TMRW

Meet UOB TMRW. The all-in-one banking app built around you and your needs. Bank. Invest. Reward. Make TMRW yours.

Find out more-

you are in Personal Banking

For Individuals

Wealth BankingPrivilege BankingFor Companies

GROUP WHOLESALE BANKINGFOREIGN DIRECT INVESTMENTAbout UOB

ABOUT USUOB GroupUOB NEWSCAREERSUSTAINABILITYUOB Subsidiaries

UOB Subsidiaries

Product Highlights

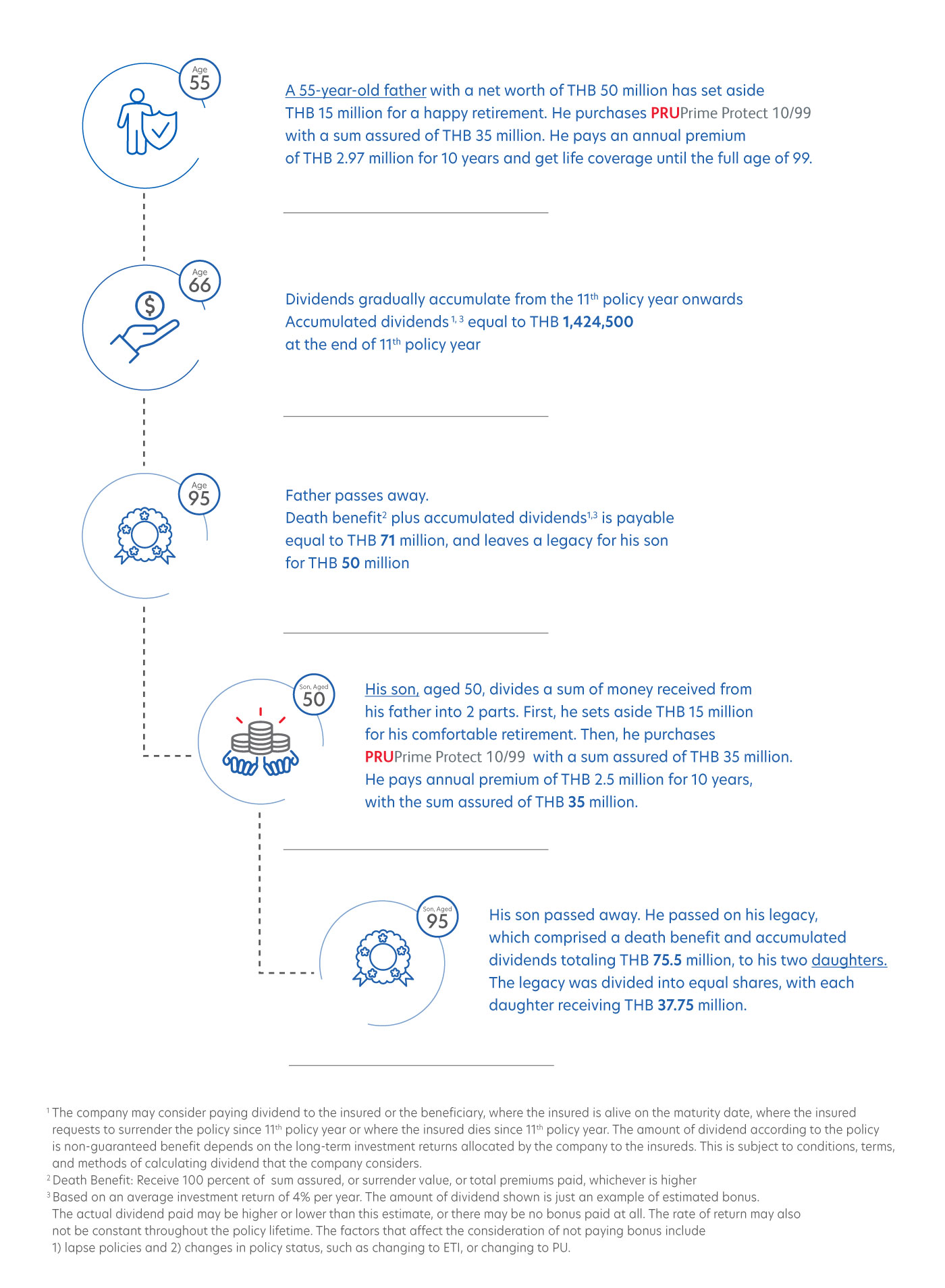

Pay premiums for only 10 years

Receive life coverage until the full age of 99 years

High life coverage of 120% of sum assured

Starting from the first policy year

Enjoy additional benefits of 150% of sum assured

from the full age of 95 years onwards

Potential to receive dividends (if any)

from 11th policy year onwards

Eligible for tax Benefits

up to THB 100,000 per year (according to conditions prescribed by the Revenue Department)

The option to purchase additional health coverage

Insured by

Table of Benefits

Coverage Benefits

|

Living Benefits

|

At the policy anniversary in which the life assured reaches the full age of 99: Receive 150% of sum assured and accumulated dividends (if any)1. |

|

Death Benefit

|

Receive between surrender value, or total premiums paid, or 120% of sum assured + accumulated dividends (if any)1, whichever is higher.

Receive between Surrender value, or total premiums paid, or 150% of sum assured, whichever is higher. + accumulated dividends (if any)1 |

|

Accumulated Dividend1

|

The company may consider paying dividend to the insured or the beneficiary, where the insured is alive on the maturity date, where the insured requests to surrender the policy since 6th policy year or where the insured dies since 6th policy year. The amount of dividend according to the policy is non-guaranteed benefit depends on the long-term investment returns allocated by the company to the insureds. This is subject to conditions, terms, and methods of calculating dividend that the company considers. |

Insurance Details

Details

Issue Age

- 1 month – 65 years

Coverage Period

- Whole life (Until the full age of 99 years)

Premium Payment Term

- 10 years

Sum Assured

- Minimum of THB 2,000,000

Mode of Premium Payment

- Annual, Semi-annual, Quarterly, and Monthly

Medical Exam

- According to the company’s underwriting criteria.

Important Notes

- This is a life insurance product. It is not a bank deposit. To get the maximum benefits from insurance policy, the insured should continuously pay the premium through to the end of the premium payment term and holds the policy until the maturity date. If the policy is terminated before the maturity date the insured may not receive benefit in the amount equivalent to the maximum benefit he/she is entitled to, or in the amount equivalent to all paid up premiums.

- A buyer should understand coverage details and conditions thoroughly before deciding to buy an insurance. Once receiving the insurance policy, please read details, terms and conditions of the policy thoroughly.

- The insured is responsible for paying premium. An insurance agent or broker that accepts a premium payment by the insured is solely for the purpose of providing service to the insured.

- The insured may cancel the policy within 15 days from the date of receiving the policy. Upon cancellation, the insured will receive a refund of the paid-up premium, minus the company’s expenses of THB 500 (if any) and the health checkup fee (if any). However, for policies proposed through electronic sales tools, the company will refund the entire premium paid without any deductions. If the insured has already exercised the right to claim compensation, they forfeit the right to cancel the policy.

- The insured has the right to surrender the policy. By doing so, they will receive the surrender value as specified in the policy value table, along with any other applicable benefits, after deducting any amounts owed to the company (if any).

- Life insurance premium, up to a maximum of THB 100,000, is entitled to annual tax deduction. A health insurance premium, up to a maximum of THB 25,000, is eligible for annual income tax deduction. However, the deduction for health premiums together with the life insurance premiums paid cannot exceed THB 100,000 in total, according to the discretion of the Revenue Department).

- “PRUPrime Protect 5” is the marketing name of “PRU Whole Life Insurance Plan 99/5 (Par)”.

The company will not cover*

- In the event of non-disclosure or misrepresentation, the company will terminate the contract within 2 years from the effective date or renewal or reinstatement of the insurance policy or the approval date to increase sum assured (only additional sum assured).

- In the event of suicide within one year from the policy effective date or renewal or reinstatement or the approval date to increase sum assured (only additional sum assured). Or the insured gets intentionally murdered by the beneficiary.

*For complete details of exclusions, please refer to the insurance policy.

Filing an insurance complaint

If you have questions about insurance or are experiencing any problem, please submit your complaint to:

- Customer Service Center Prudential Life Assurance (Thailand) Public Company Limited 944 Mitrtown Office Tower,10th, 29th - 31st Floor, Rama 4 Road, Wangmai, Pathumwan, Bangkok 10330 Tel 1621 (during office hours), email: hotline@prudential.co.th

- Any UOB Bank (PLC) branch or UOB Bank Customer Service Center 0 2285 1555 or www.uob.co.th.

- Office of Insurance Commission (OIC), Hotline 1186

- Bank of Thailand, Financial Consumer Protection Center (FCC) Hotline 1213 or fcc@bot.or.th

UOB Bank, as a licensed life insurance broker (License No. ช 00026/2545), is responsible for offering insurance products, facilitating the arrangement of life insurance contracts, and assisting with premium payments.

Prudential Life Assurance (Thailand) Public Company Limited will be responsible for all protection and benefits under terms and conditions as specified in the insurance policy.

FAQ

When are PRUPrime Protect 10/99 dividends paid out?

The company may consider paying dividend to the insured or the beneficiary, depending on the case in the following cases:

- In the case where the insured is alive on the maturity date

- In the case where the insured requests to surrender the policy since 11th policy year.

- In the case where the insured dies since 11th policy year.

The amount of dividend according to the policy is non-guaranteed benefit depends on the long-term investment returns allocated by the company to the insureds. This is subject to conditions, terms, and methods of calculating dividend that the company considers.

Does PRUPrime Protect 10/99 offer a discount on premiums?

Yes, the plan offers premium discount of THB 3 for each THB 1,000 sum assured when purchased over & above the minimum sum assured of THB 10,000,000.

Will I receive dividends if my policy converts to a reduced paid-up or extended term policy status?

No, you will not be eligible for dividends if your policy converts to a reduced paid-up or extended term policy status.

What benefits will be payable if the insured dies before the policy’s maturity date?

Death benefit: The death benefit payable during the policy term is as follows:

- The 1st policy year to the policy year in which the insured reaches the full age of 94 years: 120% of sum assured, or surrender value, or total premiums paid, whichever is higher.

- The policy year in which the insured reaches the full age of 95 – 99 years: 150% of sum assured, or surrender value, or total premiums paid, whichever is higher.

Additionally, there is the potential to receive dividends (if any) according to the company’s dividend distribution policy (From the 11th policy year onwards). Any outstanding loan balance (if any) at the time of the life assured’ death will be deducted from above the death benefit.

Can I add a rider to PRUPrime Protect 10/99 insurance plan?

Yes, there are 3 riders that can be added to this plan: 1) PRU CM Critical Illness Rider (CM), 2) Health Rider (HAW2), 3) Daily Cash Benefit Rider (HI), this HI offers coverage until age 65.

Can I add a rider to PRUPrime Protect 10/99 after paying the base premium for 5 years

Yes, you can add riders to PRUPrime Protect 10/99 if it is still in force.

Does the rider still provide coverage after the base policy is paid up?

Yes, the rider still provides coverage as long as the insured pays the rider’s premiums.

Are premiums of PRUPrime Protect 10/99 tax deductible?

Yes, premiums of life insurance plan are eligible to annual tax deduction up to THB 100,000, whereas a health insurance premium, up to a maximum of THB 25,000, is eligible for personal income tax deduction. However, the deduction for this premium together with the life insurance premiums paid cannot exceed THB 100,000 in total, according to the discretion of the Revenue Department.

Do I need a medical exam to get PRUPrime Protect 10/99?

A medical exam is required according to the company’s medical underwriting rules.

Connect with Us

UOB Contact Centre

Contact Us

Locate us

Drop your information for contact back.

Click

We use cookies to improve and customise your browsing experience. You are deemed to have consented to our cookies policy if you continue browsing our site.